When business owners ask, “What is my business really worth?” the more important question is often this: what buyers look for when buying a business.

Buyers don’t evaluate businesses the same way owners do. Owners tend to focus on years of effort, revenue growth, and personal sacrifice. Buyers, on the other hand, focus on structure, risk, predictability, and transferability. They are not buying your past. They are buying their future.

Across thousands of transactions, valuations, and due diligence processes, the same themes appear again and again. Businesses that sell well tend to align with a small set of core principles. Those that struggle usually fall short in one or more of them.

These principles closely mirror what many advisors refer to as the Seven Pillars to Profit—a framework that helps explain why some businesses attract strong offers while others face discounts, delays, or failed deals.

Below is a practical breakdown of what buyers look for when buying a business, using those seven pillars as a guide.

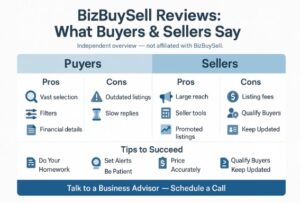

Why Buyers and Sellers Often See Value Differently

One of the biggest disconnects in a sale process is perspective.

Sellers often price based on revenue, personal workload, or what they believe the business should be worth. Buyers price based on risk, sustainability, and how easily the business can perform without the current owner.

From a buyer’s perspective, profit is only valuable if it is repeatable, defensible, and transferable. This is why two businesses with similar revenue can sell for very different prices.

Understanding this gap is the first step in understanding what buyers look for when buying a business.

The Seven Pillars Behind What Buyers Look for When Buying a Business

Pillar 1: Consistent and Defensible Profitability

Buyers don’t just look at profit. They look at the quality of profit.

They want to know whether earnings are consistent year over year and whether those earnings can reasonably continue after the ownership transition. One strong year followed by volatility raises questions. Clean trends build confidence.

Buyers also scrutinize add-backs, owner compensation, and one-time expenses. The more explanation required to justify earnings, the less reliable those profits appear.

At its core, buyers are asking: Are these profits real, and will they survive after closing?

Pillar 2: Predictable and Diversified Revenue

Another critical factor in what buyers look for when buying a business is revenue stability.

Customer concentration is one of the most common red flags in due diligence. If one client accounts for a large percentage of revenue, buyers see risk. The same applies to reliance on a single channel, vendor, or contract.

Recurring or repeat revenue is especially attractive because it reduces uncertainty. Predictability allows buyers to forecast cash flow, secure financing, and plan for growth with more confidence.

Diversified revenue streams almost always support stronger valuations.

Pillar 3: Operational Independence From the Owner

Owner dependency is one of the fastest ways to reduce buyer interest.

If the business relies heavily on the owner for sales, operations, or key relationships, buyers worry about continuity. Even motivated buyers hesitate when they feel the business cannot function without the founder.

Buyers look for documented processes, trained staff, and systems that allow the business to operate day to day without constant owner involvement. The more transferable the operations, the easier it is for a buyer to step in.

This pillar alone can significantly influence deal structure, earnouts, and transition periods.

Pillar 4: Market Position and Competitive Advantage

Buyers want to understand why customers choose your business and why they will continue to do so.

A clear market position, strong reputation, or defensible niche helps buyers justify paying a premium. Businesses that compete solely on price are harder to protect and harder to grow.

This pillar is about differentiation. Whether it’s brand strength, specialized expertise, long-term contracts, or switching costs, buyers want to see a reason your business wins consistently in the marketplace.

Strong positioning reduces competitive risk, which directly impacts valuation.

Pillar 5: Clean and Transparent Financials

Few things derail deals faster than unclear financials.

Buyers expect organized, accurate records that align with tax returns and bank statements. They want to understand margins, expenses, and trends without excessive explanation.

When financials are messy, buyers lose confidence. That loss of confidence often leads to lower offers, longer due diligence periods, or deals falling apart entirely.

Transparency builds trust, and trust is essential in every successful transaction.

Pillar 6: Scalable Growth Without Added Risk

Growth matters, but not at any cost.

Buyers value businesses that offer realistic upside without requiring extreme effort, major reinvestment, or increased personal risk. They want opportunities they can pursue after acquisition, not growth that depends on the owner working longer hours.

Scalable systems, available capacity, and logical expansion opportunities all support this pillar. Growth should feel optional and strategic, not necessary to justify the purchase.

This is a subtle but important part of what buyers look for when buying a business.

Pillar 7: Risk Reduction and Transferability

Ultimately, buyers price risk.

Legal exposure, regulatory issues, supplier dependency, outdated contracts, and aging equipment all raise concerns during due diligence. Each unresolved risk increases the likelihood of price reductions, holdbacks, or earnouts.

Buyers prefer businesses where risks are known, managed, and documented. The fewer surprises uncovered during diligence, the smoother the transaction tends to be.

Lower risk translates directly into higher confidence, stronger terms, and better outcomes for sellers.

How the Seven Pillars Framework Aligns With Buyer Thinking

Many of the factors discussed above align closely with the principles outlined in The Seven Pillars to Profit: Blueprint to Build a Business That Lasts.

The framework emphasizes building businesses that are profitable, resilient, and transferable—the same qualities buyers consistently pay for. While the book is not about selling a business specifically, its principles map directly to buyer expectations in real-world transactions.

For owners planning an eventual exit, buyers evaluating opportunities, or operators focused on long-term value creation, the framework provides a useful lens for decision-making.

You can learn more about the book here:

https://www.amazon.com/Seven-Pillars-Profit-Blueprint-Business/dp/B019SQIOMC/

Common Mistakes Owners Make When Ignoring These Pillars

Many businesses sell below expectations not because they lack revenue, but because they fail to align with buyer priorities.

Common mistakes include waiting too long to prepare, underestimating risk, overestimating goodwill, and assuming buyers will “fix things later.” In reality, buyers price problems immediately.

Understanding what buyers look for when buying a business allows owners to address weaknesses early, preserve leverage, and improve outcomes.

Final Thoughts

Profit alone does not determine value. Value is determined by how profit, operations, and risk come together in a way buyers can trust.

If you understand what buyers look for when buying a business, you gain clarity, leverage, and control—whether you plan to sell soon or years down the road.

If you’re ready to understand how buyers would evaluate your business, or what to improve before going to market, schedule a free consultation to discuss buying, selling, or improving a business.

📞 Call us today between 9 AM and 5 PM to speak directly with an experienced business advisor, or schedule a convenient time using this link — No hard sales, just honest advice. Let’s take the first step together with the right approach for a smooth, profitable experience.

strategies. Whether you’re ready to retire, explore new ventures, or simply move on, selling your landscape business at the right price and to the right buyer is crucial.

strategies. Whether you’re ready to retire, explore new ventures, or simply move on, selling your landscape business at the right price and to the right buyer is crucial. cash out, understanding the process and knowing the right steps to take is crucial. Selling a roofing company involves more than just finding a buyer—it requires careful planning, accurate valuation, and effective marketing to ensure you get the best price for your business.

cash out, understanding the process and knowing the right steps to take is crucial. Selling a roofing company involves more than just finding a buyer—it requires careful planning, accurate valuation, and effective marketing to ensure you get the best price for your business.